Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The Africa two-wheeler market encompasses the manufacture, import, distribution, and sale of motorcycles, scooters, and mopeds across the 54 nations of the African continent. This report provides a comprehensive analysis covering the period 2020–2030, with 2024 as the base year and 2021–2024 as the historical reference period. The study examines market size in value terms (USD billion), unit sales volumes, growth trends, competitive dynamics, and segment-level forecasts across vehicle type, propulsion type, and geographic dimensions.

The African two-wheeler sector has demonstrated remarkable resilience and growth, with unit sales rising from approximately 1.85 million units in 2022 to an estimated 1.99 million units in 2024. Projections indicate sales could surpass 2.32 million units by 2030, driven by the continent’s favourable demographics—Africa’s median age is under 20—rapid urbanization, and the critical role two-wheelers play in addressing mobility gaps in both urban and rural settings. The motorcycle taxi industry alone supports the livelihoods of millions of riders and transports an estimated 100 million passengers daily across East Africa. Meanwhile, the e-commerce boom is fuelling demand for two-wheelers as last-mile delivery vehicles, particularly in Nigeria, Kenya, and South Africa.

A defining characteristic of the current market is the dual-track evolution: the ICE segment continues to dominate with 98% market share, while the electric two-wheeler segment is experiencing exponential growth from a low base. Sales of electric two-wheelers surged by nearly 40% year-on-year in 2024, reaching approximately 9,000 units. Kenya’s electric motorcycle registrations rocketed from 0.5% of new sales in 2021 to 15.3% in 2025, representing one of the fastest adoption curves globally. This rapid electrification is reshaping investment flows, competitive strategies, and government policy frameworks across the continent.

Market Dynamics

Key Drivers

- Rapid urbanization and population growth: Africa’s urban population is projected to double by 2050, with cities expanding faster than public transport infrastructure. Two-wheelers fill the resulting mobility gap, particularly in congested metropolitan areas like Lagos, Nairobi, Kampala, and Addis Ababa, where they navigate gridlocked traffic and narrow streets that buses and cars cannot access efficiently.

- Commercial motorcycle taxi economy: Boda-bodas in East Africa and okadas in West Africa constitute the backbone of informal urban transport. Nigeria alone has over 8 million okadas in operation, while Kenya had over 1.4 million registered boda-bodas as of 2024. Up to 80–90% of motorcycles in Africa are used for commercial taxi, delivery, and other business applications, creating sustained replacement and expansion demand.

- Affordability advantage and microfinancing: Two-wheelers remain the most affordable motorized personal transport option in Africa, with entry-level ICE models available from USD 500–800. Financial institutions and fintech firms are expanding motorcycle financing programmes—Bajaj Auto partnered with a Nigerian fintech firm in 2023 to launch a digital motorcycle financing platform with mobile-based loan approvals and flexible repayment terms, broadening access for low- and middle-income consumers.

- E-commerce and last-mile delivery expansion: The rapid growth of e-commerce across Africa is creating significant demand for two-wheelers as delivery vehicles. Companies across the logistics and food delivery sectors depend heavily on motorcycles for fast and economical deliveries in urban centres. Platforms like Jumia, Glovo, and numerous local delivery services are scaling their two-wheeler fleets to meet rising consumer expectations for same-day and hour-based delivery.

- Electric two-wheeler cost savings: Electric motorcycles offer approximately 30–40% lower operating costs per kilometre compared to ICE counterparts. Spiro’s e-bikes in Kenya cost around USD 800—40% less than comparable gasoline models priced at USD 1,300–1,500—and riders save up to USD 3 per day on fuel and maintenance. This economic advantage is a powerful demand driver, especially for cost-sensitive commercial riders.

Key Restraints

- Limited road infrastructure and safety concerns: Inadequate road infrastructure, absence of dedicated motorcycle lanes, and limited parking facilities constrain market growth in many regions. High accident rates associated with motorcycle taxis remain a significant concern—okadas have faced partial or full bans in Nigerian cities like Lagos and Abuja due to safety and security issues, restricting market expansion in Africa’s largest economy.

- Charging infrastructure gaps for electric two-wheelers: Despite rapid progress, electric charging and battery swap infrastructure remains concentrated in a few East African markets. Outside of Kenya, Rwanda, and pockets of West Africa, grid instability and load shedding (particularly in South Africa) necessitate costly off-grid, solar-powered charging solutions that limit the scalability of electric two-wheeler adoption.

- High import duties and regulatory fragmentation: Two-wheeler manufacturers and importers face varying and often high import tariffs across African markets. The absence of harmonized standards across 54 countries creates compliance complexity, while inconsistent regulatory frameworks for motorcycle taxis create uncertainty for operators and manufacturers alike.

- Currency volatility and macroeconomic headwinds: Economic instability, currency depreciation (particularly the Nigerian naira), and fluctuating fuel prices affect both consumer purchasing power and the cost of imported two-wheelers and spare parts. Bajaj Auto, for example, has had to adjust pricing in Nigeria due to naira devaluation, impacting affordability for end consumers.

Key Trends

- Battery swapping infrastructure expansion: The battery-as-a-service (BaaS) model is emerging as the dominant business model for electric two-wheelers in Africa. Spiro operates 1,500+ swap stations across six countries, with battery swaps surging from 4 million in 2022 to over 27 million in 2025. This model eliminates range anxiety, reduces upfront vehicle costs by decoupling the battery from the bike, and enables sub-five-minute energy refills—matching or exceeding the convenience of traditional fuel stops.

- Digital ride-hailing integration: Technology platforms are formalizing the motorcycle taxi sector. SafeBoda (Uganda, Kenya), MAX (Nigeria), and Bolt have launched motorcycle ride-hailing services that introduce safety training, GPS tracking, branded equipment, and digital payment systems. MAX raised USD 24 million to finance 120,000 electric vehicles, signalling the convergence of ride-hailing and electrification strategies.

- Local assembly and manufacturing: Major manufacturers and EV startups are establishing local production facilities to reduce costs, create jobs, and benefit from preferential tariff treatment. Spiro has opened four assembly plants in Kenya, Rwanda, Uganda, and Nigeria. Roam’s 10,000-square-metre facility in Nairobi has annual capacity exceeding 50,000 motorcycles. Transsion (TankVolt), the Chinese smartphone giant, has entered the African EV market with assembly operations in Uganda, Nigeria, Kenya, Tanzania, and Ethiopia.

- Government EV policy acceleration: Kenya’s National E-Mobility Policy (2024) targets 100,000 electric motorcycles, with Kenya Power planning 400+ charging and swap stations by 2027. Rwanda targets 30% electric motorcycle penetration by 2030 and has waived import taxes on EVs. Morocco is building a USD 5.6 billion battery gigafactory set to begin production in 2026. Egypt is phasing out traditional three-wheelers in favour of electric alternatives under its National Automotive Manufacturing Programme.

Market Segmentation

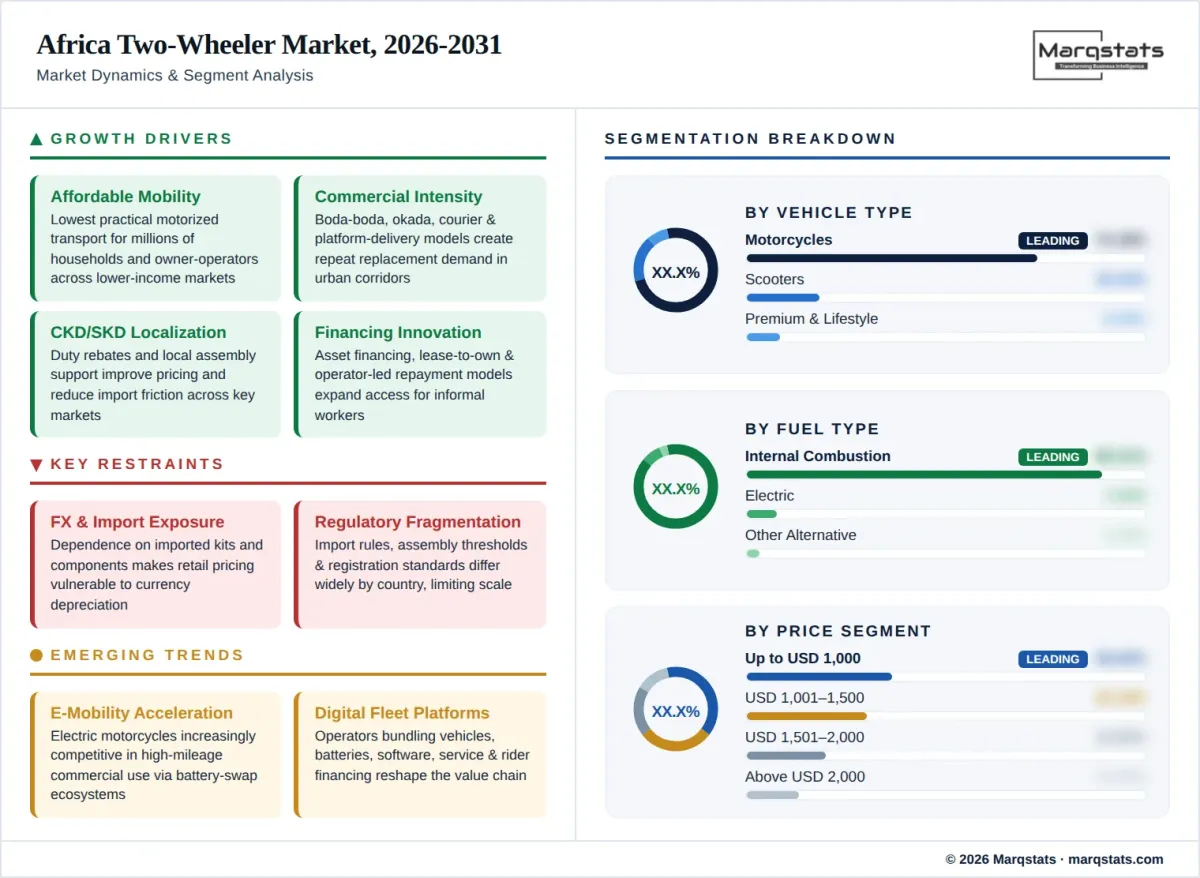

Motorcycles constitute the dominant vehicle type in the Africa two-wheeler market, commanding over 75% of total market revenue in 2024. Standard motorcycles in the 100–250cc range account for 48.5% of the overall two-wheeler market, driven by their versatility for both personal commuting and commercial use. Bajaj Boxer, Honda ACE110, TVS Star HLX, and Yamaha Crux are among the best-selling models, offering durability, fuel efficiency, and low maintenance costs suited for Africa’s diverse terrain. The motorcycle segment benefits from well-established distribution networks of Indian and Japanese OEMs, extensive spare parts availability, and the sheer scale of the motorcycle taxi economy.

Scooters and mopeds represent a smaller but growing segment, particularly in North African markets (Morocco, Egypt, Algeria) and urban centres of South Africa. These vehicles appeal to urban commuters seeking convenience, automatic transmission, and easy manoeuvrability in city traffic. The segment is expected to gain traction as urbanization intensifies, more women enter the rider demographic, and electric scooter models become available at competitive price points. Piaggio’s Vespa brand, Sym, and Kymco maintain presence in this segment, alongside emerging Chinese manufacturers offering low-cost alternatives.

The ICE segment commands approximately 98% of the Africa two-wheeler market as of 2024 and will remain dominant through the forecast period, albeit with a declining share. ICE two-wheelers benefit from established fuel distribution infrastructure, lower upfront purchase prices for basic models, widespread service and maintenance networks, and consumer familiarity. The segment’s strength is reinforced by the robust presence of Bajaj Auto (whose Boxer model maintains over 40% market share in Nigeria), Honda, TVS, and Yamaha, who have invested heavily in Africa-specific product development. However, rising fuel costs, stricter emissions standards, and the growing cost competitiveness of electric alternatives are gradually eroding the ICE segment’s dominance.

Electric two-wheelers represent the fastest-growing segment in the Africa two-wheeler market, with sales surging by nearly 40% year-on-year in 2024 to approximately 9,000 units. Kenya leads the electrification charge—electric motorcycles accounted for 15.3% of all new registrations in 2025 (25,277 out of 168,286 units), up from just 0.5% in 2021. The segment is dominated by African-born startups and new entrants: Spiro (60,000+ deployed bikes across six countries), Roam (50,000-unit annual production capacity), and Ampersand (5,700+ e-motos, 70% market share in Rwanda). The battery swapping model has proven transformative, addressing range anxiety and high upfront costs simultaneously. Electric two-wheelers are projected to capture over 50% of all motorcycle sales in Africa by 2040, driven by falling battery costs, expanding swap infrastructure, and government incentive programmes.

Commercial use dominates the Africa two-wheeler market, with an estimated 80–90% of motorcycles deployed for taxi services, ride-hailing, delivery, and other business applications. Motorcycle taxis serve as the primary mode of motorized transport in much of East and West Africa, moving 60–75% of motorized passengers and goods in many African cities. The commercial segment is the primary target for electric two-wheeler companies, as taxi riders are highly sensitive to operating costs and typically cover 80–150 km per day, maximizing the fuel savings advantage of electric powertrains.

Personal use accounts for a smaller but significant share of the market, particularly in North Africa (Morocco, Egypt, Algeria) and South Africa where recreational, commuting, and touring riding are more prevalent. Rising disposable incomes among Africa’s emerging middle class, growing interest in adventure and touring motorcycles, and increasing female ridership are expanding the personal use segment. Premium brands such as BMW Motorrad, KTM, and Harley-Davidson maintain a niche presence catering to lifestyle and recreational riders, primarily in South Africa and North African markets.

By Geography

West Africa

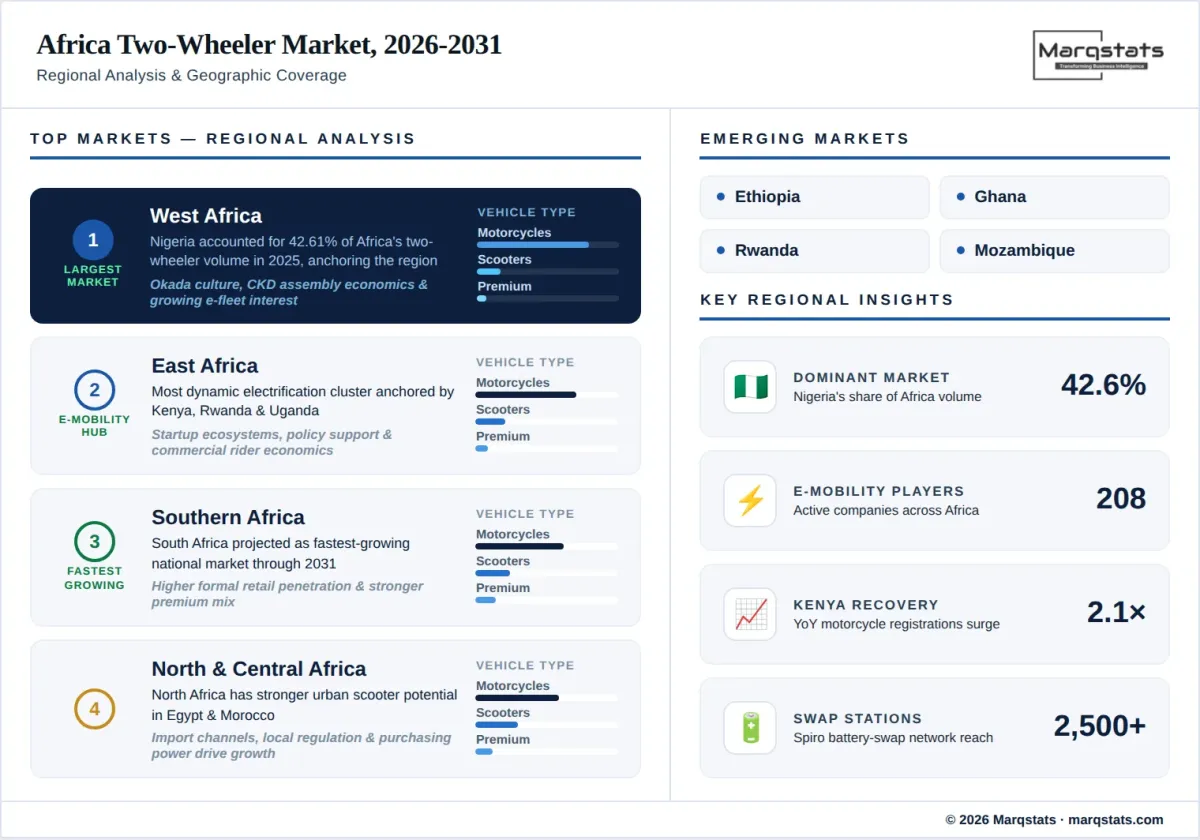

West Africa is the largest regional market for two-wheelers in Africa, anchored by Nigeria—the continent’s single largest two-wheeler market with 28.4% of total regional revenue. Nigeria imports over 800,000 motorcycles annually through official channels, with an additional 200,000 estimated through informal routes. The okada economy sustains millions of livelihoods, with over 8 million commercial motorcycles on Nigerian roads. Bajaj Auto commands a leading position, exporting approximately 500,000 units annually to Nigeria, while Honda holds approximately 27% unit sales share. Ghana is also an emerging market, with the government’s proposed revision of Legislative Instrument 2180 to formalize and regulate the okada sector marking a significant policy shift. West Africa lags behind East Africa in electric two-wheeler adoption, but its sheer market scale—Nigeria alone sells over 1 million motorcycles annually—makes it the region to watch for electrification impact.

East Africa

East Africa is the continent’s fastest-growing regional market and the global epicentre of two-wheeler electrification. Kenya leads with over 1.4 million registered boda-bodas and an annual growth trajectory of approximately 250,000 new motorcycles per year. The country hosts 50+ e-mobility startups, including Roam, Ampersand Kenya, Kiri EV, and Spiro. Kenya’s National E-Mobility Policy (2024) targets 100,000 electric motorcycles, with Kenya Power planning 400+ charging and swap stations by 2027. Rwanda has emerged as an early EV policy leader, waiving import taxes on electric vehicles and targeting 30% electric motorcycle penetration by 2030. Ampersand holds 70% EV market share in Rwanda with over 2,200 bikes sold. Uganda and Tanzania feature strong boda-boda markets with growing pilot programmes from Zembo, GOGO Electric, and other startups. Ethiopia is attracting new entrants like Dodai and Chinese manufacturer Yidea.

North Africa

North Africa represents a distinct market profile, with Morocco, Egypt, and Algeria as the primary markets. Morocco has positioned itself as Africa’s leading passenger vehicle exporter, surpassing one million units produced in 2025, and aims for 60% of its vehicle production capacity to be electric by 2030. A USD 5.6 billion battery gigafactory under construction is set to begin production in 2026, providing a component backbone for emerging electric scooter and motorcycle fleets. Egypt is aggressively localizing EV assembly under its National Automotive Manufacturing Programme, phasing out traditional three-wheelers (tuk-tuks) in favour of electric alternatives and launching locally-made electric motorcycles like the Kader, priced at approximately USD 1,800. Algeria has a sizeable two-wheeler market driven by commuter demand but faces limited EV infrastructure development compared to its regional peers.

Southern Africa

South Africa is the most developed two-wheeler market in the region, characterized by higher purchasing power, stronger infrastructure, and greater consumer preference for premium and mid-range motorcycles. The market features robust presence of international brands in the adventure, touring, and recreational segments. However, South Africa’s EV transition faces headwinds from a 25% EV import tax and chronic load shedding that undermines grid reliability for charging infrastructure. Despite these challenges, the country’s well-established automotive manufacturing base and growing environmental consciousness present medium-term opportunities for two-wheeler electrification. Other Southern African nations like Mozambique, Zambia, and Zimbabwe represent nascent but growing markets, primarily driven by commercial motorcycle use.

Central Africa

Central Africa remains an emerging market for two-wheelers, with the Democratic Republic of Congo and Cameroon as the primary demand centres. The region features predominantly ICE-powered motorcycles used for commercial transportation in both urban and rural settings. Infrastructure challenges, political instability in some markets, and limited formal distribution networks constrain growth. However, Spiro has launched pilot programmes in Cameroon and Tanzania, signalling growing interest from electric mobility players in expanding beyond established East and West African markets.

How Competition Is Evolving

The Africa two-wheeler market is moderately fragmented, with the top five companies—including Honda Motor Co., Bajaj Auto, TVS Motor Company, Yamaha Motor Co., and Hero MotoCorp—collectively accounting for approximately 50% of the market. Indian manufacturers hold a particularly strong position, leveraging their cost-competitive manufacturing base, Africa-specific product development, and extensive distribution partnerships. Bajaj Auto’s Boxer model has achieved iconic status in West Africa, maintaining over 40% market share in Nigeria through its combination of durability, fuel efficiency, and affordability. Honda maintains the highest unit sales share in Nigeria at 27.2%, supported by an extensive dealer and service network across major markets.

The competitive landscape is undergoing rapid transformation with the entry of electric two-wheeler companies. Spiro has emerged as Africa’s largest EV company, having raised over USD 280 million in total funding and deploying 60,000+ e-bikes with 1,500 swap stations across six countries. Roam (formerly Opibus), a Swedish-Kenyan manufacturer, has secured USD 24 million in Series A funding and built a 50,000-unit capacity facility in Nairobi. Transsion, the Chinese company behind Africa’s leading smartphone brands (Tecno, Infinix), has entered the market with its TankVolt electric two-wheeler brand, leveraging its unparalleled distribution infrastructure across the continent. These new entrants compete not just on vehicle price but on integrated mobility ecosystems that include battery swapping, digital financing, and fleet management platforms.

Competitive strategies in the market increasingly centre on local assembly operations, digital financing partnerships, and integrated energy service models. Companies are forming joint ventures with local partners, investing in after-sales service networks, and developing pay-as-you-go models that make two-wheeler ownership accessible to a broader consumer base. Mergers and acquisitions activity has been relatively moderate compared to other global regions, with partnerships and organic expansion being the preferred growth strategies. The convergence of ride-hailing technology, electric powertrains, and battery-as-a-service models is creating a new competitive paradigm that favours vertically integrated players capable of delivering end-to-end mobility solutions.

Companies Covered

The report profiles 18++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides a comprehensive analysis of the Africa two-wheeler market covering the period 2020–2030, with 2024 as the base year. The study examines market size and growth trends in value terms (USD billion), unit sales volumes, competitive landscape dynamics, and segment-level forecasts across vehicle type (motorcycles, scooters/mopeds), propulsion type (ICE, electric), end use (commercial, personal), and geographic dimensions covering West Africa, East Africa, North Africa, Southern Africa, and Central Africa. Country-level analysis is provided for Nigeria, Kenya, South Africa, Egypt, Ethiopia, Morocco, Ghana, Uganda, Tanzania, Angola, Rwanda, and Algeria.

Primary research includes analysis of industry databases, government statistical agencies, trade bodies, and company disclosures. Secondary research draws from national statistics bureaus (Nigerian Bureau of Statistics, Kenya National Bureau of Statistics), industry associations, multinational development organization reports, trade publications, patent filings, and corporate annual reports. The report profiles 18 key companies, including leading ICE manufacturers and emerging electric two-wheeler players, and examines their competitive strategies, product portfolios, and market positioning within the African context.