Market Snapshot

Key Takeaways

Market Overview & Analysis

Report Summary

The India electric car market encompasses passenger vehicles powered entirely or partially by electricity, including battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs). This market segment includes vehicle manufacturers, battery producers, charging infrastructure providers, and associated service providers. The market analysis covers the period from 2026 to 2031, with 2024 serving as the base year and historical data spanning 2021-2024.

India's electric car market is transitioning from early adoption to mainstream acceptance, supported by a confluence of policy incentives, technological advancement, and evolving consumer preferences. The market recorded approximately 176,817 electric car sales in CY2025, representing 77% year-on-year growth and achieving an all-time high. Electric vehicle penetration reached approximately 4% of total passenger vehicle sales, up from 2.5% in 2024, with the government targeting 30% EV share by 2030. The market is characterized by strong domestic manufacturing presence, with Tata Motors, Mahindra & Mahindra, and MG Motor commanding the majority of sales volumes.

The competitive landscape has transformed significantly, with Tata Motors' market share declining from 73% in 2023 to approximately 40% in 2025 as competitors launched aggressive product portfolios. Mahindra's born-electric SUVs (BE 6 and XEV 9e) achieved 369% sales growth in CY2025, while MG Motor's Windsor EV captured significant market share with its attractive pricing and battery-as-a-service model. The entry of Tesla in July 2025 and the expansion of BYD, alongside upcoming launches from Maruti Suzuki (e-Vitara) and Hyundai (Creta Electric), signals intensifying competition that will benefit consumers through improved products and competitive pricing.

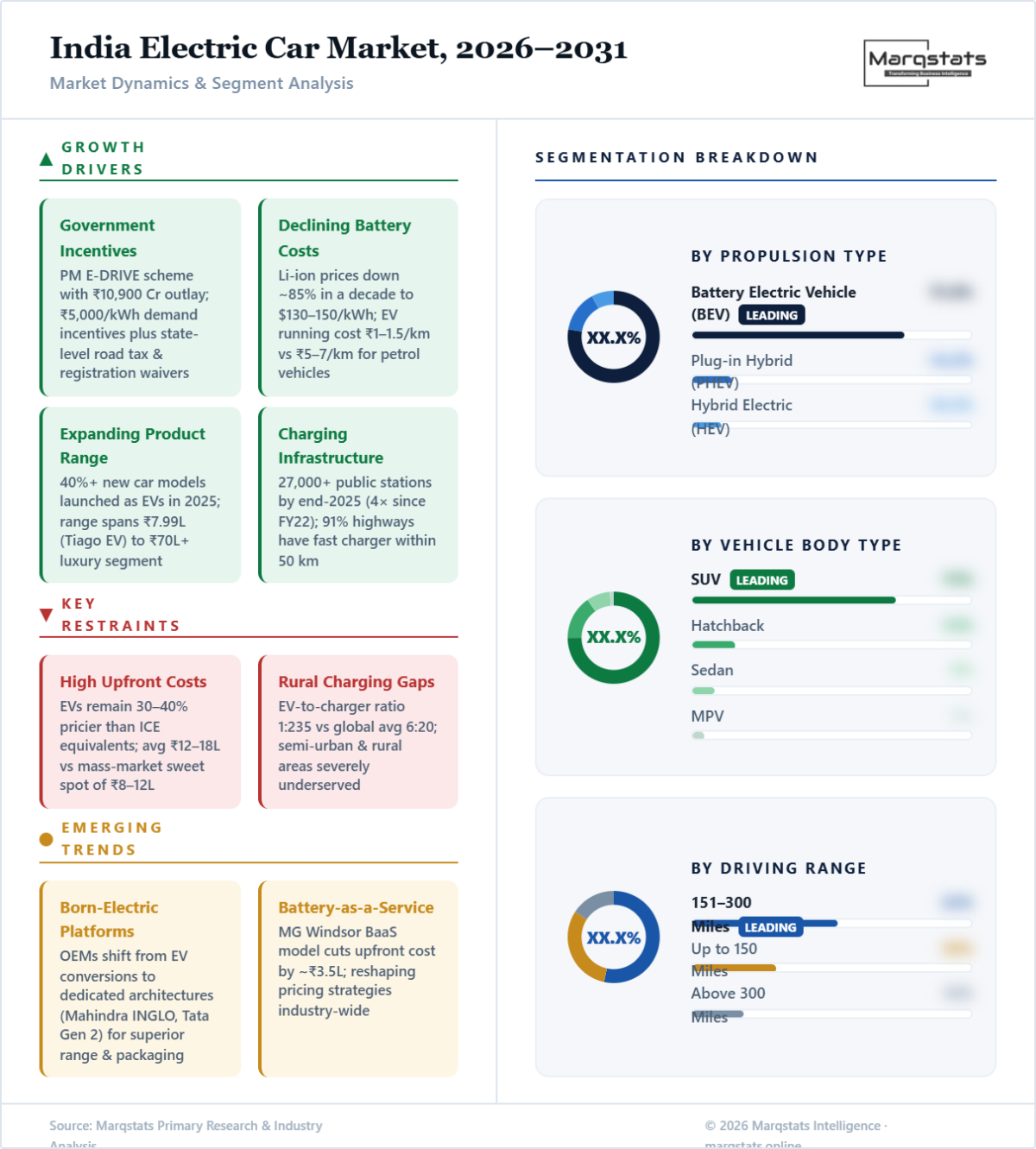

Market Dynamics

Key Drivers

- Government Policy Support and Incentives: The PM E-DRIVE scheme (October 2024-March 2026) with Rs 10,900 crore allocation provides demand incentives of Rs 5,000/kWh for EVs, while state governments offer additional benefits including road tax waivers, reduced registration fees, and parking incentives. The scheme targets procurement of over 14,000 e-buses and establishment of 72,000 charging stations.

- Declining Battery Costs and Total Cost of Ownership: Lithium-ion battery prices have declined approximately 85% over the past decade, reaching USD 130-150 per kWh by 2024. This cost reduction, combined with lower running costs (electricity vs. fuel) of approximately Rs 1-1.5 per kilometer for EVs versus Rs 5-7 for petrol vehicles, makes electric cars increasingly economical over the vehicle lifecycle.

- Rising Fuel Prices and Environmental Awareness: Increasing petrol and diesel prices, combined with growing consumer awareness of air pollution and climate change, drive preference for zero-emission vehicles. Urban air quality concerns in major cities including Delhi, Mumbai, and Bangalore have heightened demand for cleaner transportation solutions.

- Expanding Product Portfolio and Improved Technology: Launch of over 40% of new car models as EVs in 2025, with improved driving ranges (150-500+ km), faster charging capabilities, and advanced features including connected car technology. The availability of electric vehicles across price segments from Rs 7.99 lakh (Tata Tiago EV) to Rs 70+ lakh (luxury segment) expands addressable market.

- Charging Infrastructure Expansion: Public charging network expanded to over 27,000 stations by end-2025, representing a fourfold increase since FY22. Maharashtra, Delhi, and Karnataka lead deployment, with 91% of highways now having a fast charger within 50 km, addressing range anxiety concerns.

Key Restraints

- High Upfront Costs: Electric vehicles remain 30-40% more expensive than comparable ICE vehicles at the point of purchase. The average electric car price of Rs 12-18 lakh remains above the Rs 8-12 lakh sweet spot for mass-market adoption in India, limiting penetration among price-sensitive consumers.

- Inadequate Charging Infrastructure in Non-Metro Areas: While urban centers have seen significant infrastructure expansion, rural and semi-urban areas remain underserved. India's EV-to-charger ratio of 1:235 (as of July 2025) remains well below the global average of 6:20, creating persistent range anxiety, particularly for intercity travel.

- Battery Safety Concerns: Incidents of EV battery fires have raised consumer concerns about vehicle safety. While incidents remain statistically rare, negative publicity has impacted consumer confidence, prompting the Bureau of Indian Standards to introduce new safety standards in June 2024.

- Supply Chain Dependencies: India remains reliant on imported lithium-ion cells, predominantly from China, exposing the market to supply chain disruptions and currency fluctuations. Domestic cell manufacturing under the PLI-ACC scheme has faced delays, with none of the beneficiaries meeting December 2024 milestones.

Key Trends

- Rise of Born-Electric Platforms: OEMs are transitioning from EV conversions to dedicated electric vehicle platforms (e.g., Mahindra INGLO, Tata's Gen 2 architecture) offering superior packaging, performance, and efficiency. These purpose-built platforms enable longer range, faster charging, and better utilization of interior space.

- Battery-as-a-Service (BaaS) Models: MG Motor's Battery-as-a-Service model for the Windsor EV, reducing upfront costs by approximately Rs 3.5 lakh, is gaining traction. This model addresses upfront cost concerns while providing flexibility for battery upgrades, potentially reshaping pricing strategies across the industry.

- Premiumization and SUV Dominance: The electric car market is witnessing a shift towards premium SUVs, with the segment accounting for 73% of sales. Consumers are increasingly choosing feature-rich models in the Rs 15-25 lakh range, with driving range and performance becoming key differentiators over price alone.

- Domestic Battery Manufacturing Push: Major investments in lithium-ion cell manufacturing by Tata Group (USD 1.5 billion gigafactory), Exide Industries, and Amara Raja under the PLI-ACC scheme aim to reduce import dependency. Commercial production is expected from 2026, potentially reducing battery costs by 15-20%.

Market Segmentation

Battery electric vehicles dominate the India electric car market with approximately 75.6% market share in 2024-2025. The segment is driven by zero tailpipe emissions, lower running costs, and strong alignment with government incentives under the PM E-DRIVE scheme. Key models including Tata Nexon EV, Tata Punch EV, MG Windsor, and Mahindra BE 6 lead sales volumes. The segment is projected to maintain dominance throughout the forecast period as charging infrastructure expands and battery costs continue declining.

The PHEV segment remains nascent in India but is expected to grow at a significant CAGR during the forecast period. These vehicles address range anxiety concerns by combining electric and internal combustion powertrains. While currently limited to luxury segments (BMW, Volvo), mass-market PHEV launches from Toyota and Maruti Suzuki are expected to expand the segment. PHEVs are particularly suited for consumers transitioning from ICE vehicles who require flexibility for long-distance travel.

The SUV segment commands approximately 73% of India's electric car market, reflecting strong consumer preference for larger, feature-rich vehicles. Key models include Tata Nexon EV, Tata Punch EV, MG ZS EV, Mahindra BE 6, Mahindra XEV 9e, and Hyundai Creta Electric. The segment benefits from the ability to accommodate larger battery packs enabling longer driving ranges, while offering the road presence and utility Indian consumers prefer. Premium SUVs in the Rs 18-30 lakh range are the fastest-growing sub-segment.

The hatchback segment serves as the entry point to electric car ownership, led by models like Tata Tiago EV (starting Rs 7.99 lakh) and MG Comet EV. While smaller in absolute volume compared to SUVs, this segment is crucial for mass-market adoption and is expected to grow as new launches target the sub-Rs 15 lakh price point. The segment's growth is closely tied to government subsidies and emerging battery-as-a-service models that reduce upfront costs.

The sedan segment holds a smaller market share, primarily concentrated in the premium segment with models like BYD Seal. Traditional sedan demand in India has declined in favor of SUVs, and this trend extends to the EV segment. However, premium sedans offer differentiated driving dynamics and are expected to maintain a niche presence, particularly as Tesla expands its India footprint with the Model Y and potentially Model 3.

This range segment held the maximum market share in 2024-2025, with popular models from Tata, Mahindra, and MG falling within this category. These vehicles, priced between USD 7,000-30,000, align with the purchasing power of India's broad buyer base while offering sufficient range for daily commuting and occasional intercity travel. The segment benefits from the optimal balance of battery size, vehicle weight, and cost.

Premium models including Tata Harrier EV (up to 627 km range), Mahindra XEV 9e, and Tesla Model Y target consumers prioritizing range confidence. This segment is growing as battery technology improves and charging infrastructure gaps persist in certain regions. The longer range reduces dependence on public charging, making EVs more practical for consumers in areas with limited infrastructure.

By Geography

Maharashtra

Maharashtra leads India's electric car market with significant concentration in Mumbai, Pune, and Nagpur. The state benefits from a comprehensive EV policy offering road tax exemptions, registration fee waivers, and subsidies for charging infrastructure. Mumbai's metro area accounts for the highest electric car registrations nationally, driven by high per capita income, strong environmental awareness, and urban mobility challenges. The presence of major corporate headquarters and fleet operators further accelerates adoption. Maharashtra's charging infrastructure is among the most developed, with leading deployment of public charging stations.

Delhi National Capital Region

Delhi NCR represents the second-largest market for electric cars in India, driven by severe air pollution concerns, aggressive state EV policies, and high consumer purchasing power. The Delhi EV Policy offers purchase subsidies, road tax exemptions, and waiver of registration fees. The region's charging infrastructure has expanded significantly, supported by government initiatives and private investments from Tata Power, Statiq, and other charge point operators. Gurgaon and Noida are emerging as key demand centers, particularly for premium EVs.

Karnataka

Karnataka, led by Bangalore, is a leading electric vehicle market benefiting from its status as India's technology hub. The state was first to adopt a dedicated EV policy in 2017, offering concessional land leases for charging infrastructure and strong policy coordination through BESCOM. High concentration of IT professionals with global exposure and environmental consciousness drives demand. The state leads in public charging infrastructure deployment, with strategic placement along corridors including the Bangalore-Mysore Expressway and Bangalore-Chennai Highway.

Tamil Nadu

Tamil Nadu is emerging as a key market, particularly with the establishment of EV manufacturing facilities by Hyundai, Ola Electric, and VinFast. Chennai's industrial ecosystem and port connectivity make it attractive for EV production and supply chain development. The state EV policy offers incentives for manufacturing and charging infrastructure deployment. Consumer adoption is concentrated in Chennai and Coimbatore, with growing penetration in Tier-2 cities.

Rest of India

Gujarat, Uttar Pradesh, Telangana, and Kerala are emerging as significant markets. Gujarat benefits from its strong auto manufacturing base (Tata Motors Sanand plant, battery gigafactories) and proactive state EV policy. Uttar Pradesh has seen rising adoption in Lucknow, Noida, and Agra, supported by state subsidies. Kerala shows high adoption rates relative to its size, driven by environmental consciousness and high literacy rates. Bihar, despite ranking fifth in EV sales nationally with 113,000+ registrations in FY2025, faces infrastructure constraints limiting electric car adoption specifically.

How Competition Is Evolving

The India electric car market is moderately concentrated, with the top three players—Tata Motors, MG Motor India, and Mahindra Electric—commanding approximately 88% of market share in CY2025. However, the competitive intensity has increased dramatically, with Tata Motors' dominance declining from 73% share in 2023 to approximately 40% in 2025 as competitors launched aggressive product portfolios. The market is witnessing a shift from Tata's early-mover advantage to a more competitive three-way battle for leadership.

Competitive strategies center on product differentiation, pricing innovation, and ecosystem development. MG Motor disrupted the market with its battery-as-a-service model for the Windsor EV, reducing upfront costs significantly. Mahindra's born-electric INGLO platform vehicles (BE 6, XEV 9e, XEV 9S) offer premium positioning with advanced technology. Tata Motors maintains the broadest portfolio spanning entry-level (Tiago EV, Rs 7.99 lakh) to premium (Harrier EV, Rs 28.99 lakh), leveraging its extensive dealer network and manufacturing scale.

Global entrants are reshaping competitive dynamics. Tesla's India entry in July 2025 brings premium brand appeal and advanced technology, while BYD has achieved 88% sales growth by targeting the accessible luxury segment. Upcoming launches from Maruti Suzuki (e-Vitara), Hyundai (Creta Electric), Toyota, Kia, and VinFast will further intensify competition. The market is expected to witness consolidation of positioning around distinct segments: value (Tata, Maruti), mainstream premium (Mahindra, MG, Hyundai), and luxury (Tesla, BMW, Mercedes-Benz, BYD).

Companies Covered

The report profiles 16++ companies with full strategy and financials analysis, including:

Recent Market Activity

Table of Contents

Coverage & Segmentation

This report provides comprehensive analysis of the India electric car market covering the forecast period 2026-2031, with 2024 as the base year and historical analysis spanning 2021-2024. The study examines market size, growth trends, competitive landscape, segment-level analysis, and regional distribution across India. The market scope includes battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs) in the passenger car segment, excluding commercial vehicles and two/three-wheelers.

Primary research includes analysis of vehicle registration data from the VAHAN portal (Ministry of Road Transport and Highways), industry stakeholder perspectives, and OEM announcements. Secondary research draws from government databases including Ministry of Heavy Industries, Ministry of Power, NITI Aayog, industry bodies (SIAM, FADA, SMEV), company annual reports and investor presentations, trade publications, and proprietary databases. Market sizing employs bottom-up analysis validated against top-down estimates using registration data, production figures, and import statistics.